With an increase of new cases of coronavirus (COVID-19) in the US and community spread more likely throughout the country, there could be a slowdown in economic activity of businesses and individuals. As we monitor the effects of COVID-19 on the overall bond market and credit quality, we are reminded of the significant amount of interconnection throughout our country’s and the world’s economy. The focus of this bulletin is to highlight municipal bond sectors that may be most impacted by a sustained economic slowdown. These are the sectors that we are targeting for scrutiny and depending on the path that the COVID -19 takes, this list could broaden. However, we do want to note that as part of our risk management, we seek to construct portfolios with very strong credits, taking into account sector and revenue diversification.

- Airports and Ports: With many businesses and individuals reducing travel and tourism, both abroad and domestically, airport revenues could decline. Direct airline revenues will not be the only source of revenue affected, as we will likely see reduced concessions such as parking and food services. Airports do have strong liquidity as a sector, with the 2019 Moody’s Medians showing 659 days cash on hand, which would help weather short term declines in enplanements. In late February we undertook a comprehensive review of our airport exposures and began trimming portfolios with the highest exposures to this sector. An extended slowdown could have a negative impact on both the supply chain and demand side for goods, which would be felt at ports.

- Tax Secured Bonds: State and local governments issue bonds backed by specific dedicated taxes, including sales and income tax. Although a sustained economic slowdown could reduce collections of those taxes, debt service coverage has been strong for the past few years, so again, it would take a prolonged downturn to materially affect coverage. Taxes that are less broad-based, such as hotel occupancy or gas taxes could be impacted more quickly. We want to note that most of the bonds that our clients hold have the broader income and/or sales tax pledge.

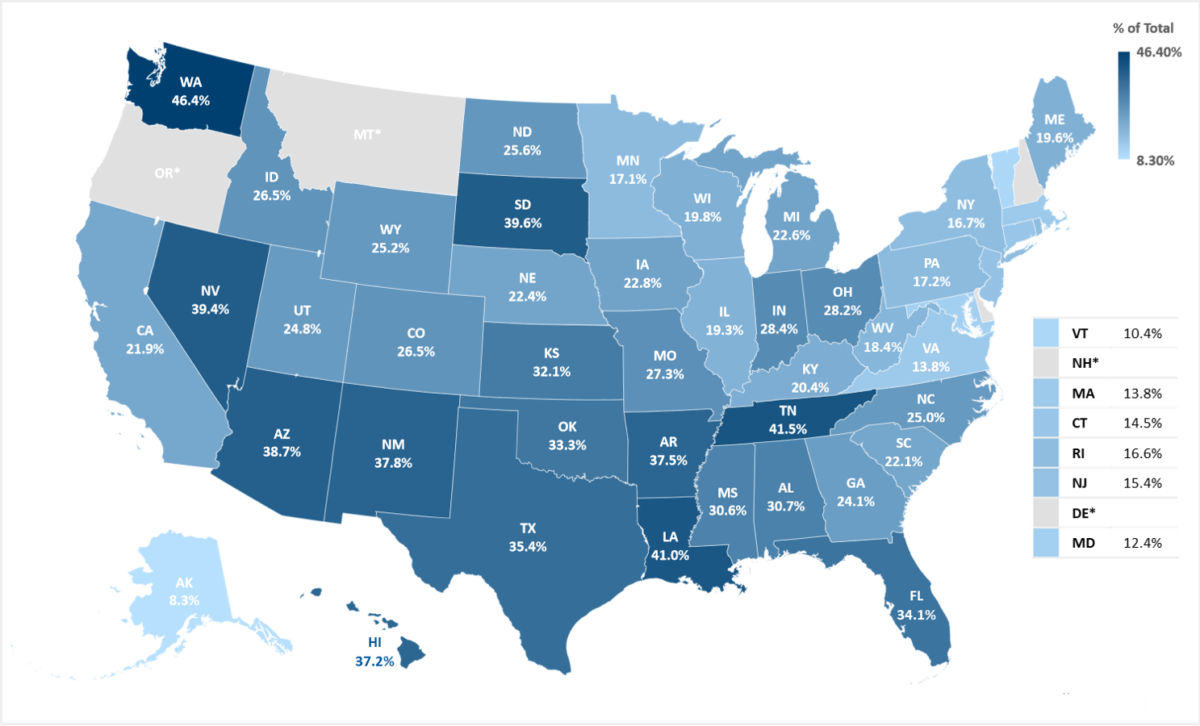

Sales Tax Collections as a Percent of Total State and Local Tax Collections

Note: *Delaware, Montana, New Hampshire, and Oregon levy neither a state nor a local sales tax.

Source: Census Bureau, Tax Foundation calculations Fiscal Year 2016.

- Mass Transit. A decline in economic activity could reduce mass transit ridership, however, most mass transit issuers have multiple revenue sources including sales tax or transportation related fees such as license renewals or gas tax. We believe this diversity of revenues should withstand a short-term shock. On the other side, a decline in mass transit may be coupled with an increase in individual car usage, which could increase gas taxes.

- Health Care: Hospitals could face multiple challenges should COVID-19 become widespread. These challenges include updating and training staff on how to deal with preparedness, adequate supplies, infection control, allocation of patient beds, changes in admission patterns including reducing elective procedures and other concerns. It is a credit positive that more hospitals are parts of systems (2/3 in 2020, up from 58% ten years ago), so best practices and information can be more easily shared.

- State and Local Government Taxes: The map below shows state dependency on sales tax. The 5 states that are most dependent on sales tax for their state budgets include Washington, Tennessee, Louisiana, South Dakota and Nevada. These states may see a greater impact of declining economic activity if the spread of coronavirus is sustained.

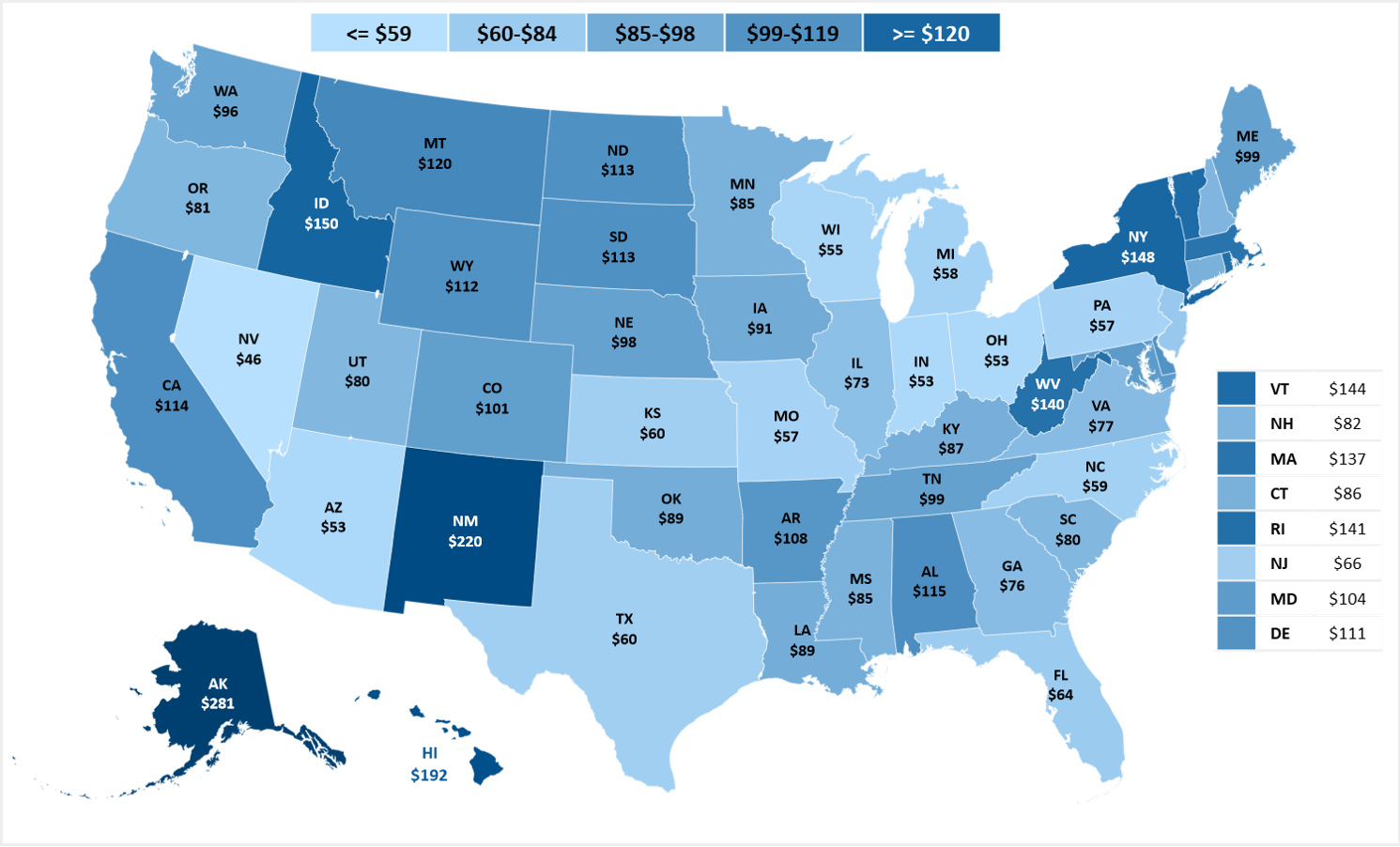

Public health is one of the main responsibilities of state and local governments, as it aims to proactively have initiatives and programs that improve overall health in communities. There are a wide range of programs, with prevention of chronic and infectious diseases amongst them. This map shows public health spending by state in 2019, exclusive of Medicaid dollars. The degree of public spending reflects, in part, the political priorities that a state bases on public health and may give some indication of state preparedness for public health crises.

State and local governments do not operate in a vacuum in a crisis situation. The US has shown time and again that when disasters strike, money flows into the places and sectors most affected, and we expect it would happen again if appropriate. Fiscal and monetary policy can and has been used in the past to deliver on public policy objectives. We will continue to update you as this fluid situation develops.

Public Health Funding by State: State dollars dedicated to public health and federal dollars directed to states per person

Source: Trust for America’s Health; U.S. HHS; U.S. Census Bureau, Annual Estimates of the Resident Population: April 1, 2010 to July 1, 2018, 2017-2018

You can find Fiera Capital’s latest analysis and updates on COVID-19 by clicking here.

Global Asset Allocation Team Market Update – November 2025

The fourth quarter got off to a strong start. Solid economic and corporate earnings results in the United States provided a tailwind for global stock markets – while a tentative trade truce between the United States and China added to the optimistic mood in the market.

Learn more Global Asset Allocation Team Market Update – November 2025